Medicare IRMAA Surcharges and 5 Ways to Avoid Them

IRMAA stands for Income-Related Monthly Adjusted Amount. It is an increase to the standard Medicare Part B and Part D monthly premiums that Medicare recipients have to pay each month if they make over a certain amount.

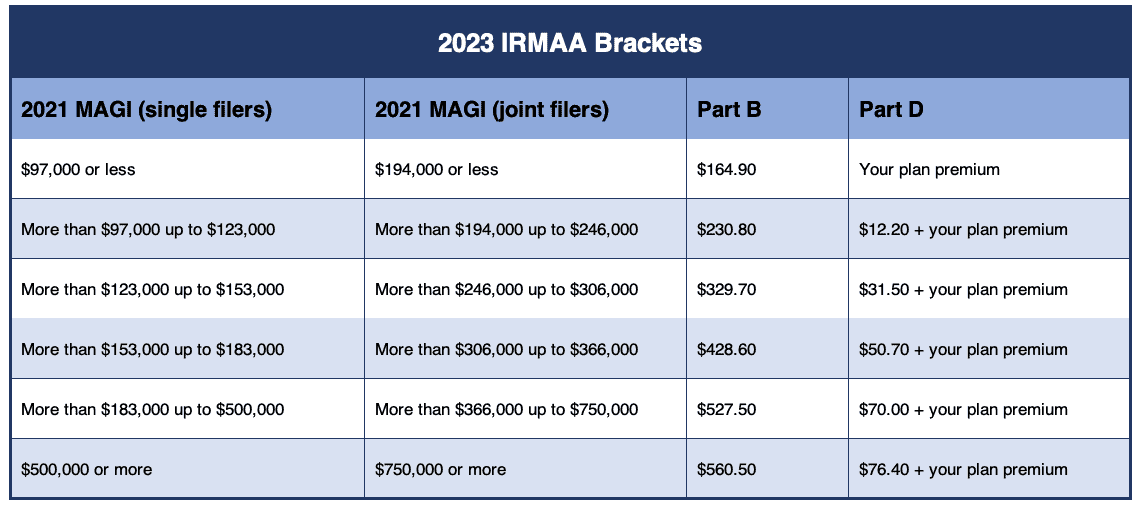

For 2023, the standard Part B premium is $164.90/month and Part D is $0 (plus your plan premium). Depending on your income, your Part B premiums can go up to $560/month and Part D can go up to $76/month.

These pesky surcharges are based on hard limits, where $1 over, causes an increase in premium. This can lead to a lot of frustration because, with proper planning, most retirees can adjust their income up or down a bit from year to year using a few strategies discussed below.

1) Qualified Charitable Distributions or QCDs are a strategy where you gift directly from your pre-tax retirement account to charity. In order to make this gift you have to be over the age of 70 ½. If you are subject to required minimum distributions (RMD), QCDs can satisfy a portion of your RMD and reduce your MAGI. Other forms of charitable gifting such as cash gifts will not reduce your Medicare premiums because they are a below-the-line deduction.

Here’s an example. Bob and Jane give $5,000/year to charity. They also have IRAs that have required minimum distributions of $40,000 in 2022. They gift $5,000 of the RMD tax-free to charity.

2) Withdrawing from after-tax sources is helpful for those right at the Medicare income thresholds. For example, if Bill and Jane normally withdraw $5,000/month from their IRAs but realize in November that their December distribution will increase their AGI from $192,000 to $197,000, taking them over the $194,000 threshold, they might decide to skip the December distribution and if they need the money take it from cash savings, a Roth IRA, a HELOC, or another after-tax source.

3) Using tax-efficient investments in taxable accounts. Directing more of your tax-efficient investments, such as dividend-paying stocks, taxable bonds, and active mutual funds with capital gain distributions to your IRAs or Roth IRAs can reduce your income since those accounts are tax-advantaged.

4) Roth conversions are a great way to reduce your future tax liability. Take for example a retired couple who are both 67 and have to begin RMDs in 6 years at the age of 73. Without RMDs, they project their AGI to be $140,000. With RMDs ($60,000/year) they expect their AGI to be $200,000, over the $194,000 limit. They begin doing Roth conversions and over the next 4 years reduce their pre-tax retirement accounts by 25%, lowering the expected RMD to $45,000 ($60,000 x 75%). Now their expected AGI when they begin taking RMDs is $185,000, below the $194,000 threshold.

5) Appeal the decision through Form SSA.44. Social Security considers the following, among others, to be events that may warrant an appeal –

a. Death

b. Marriage/Divorce

c. Stopping work or less work (retirement for example)

d. Involuntary loss of income-producing property (depends on the reason for loss)

e. Loss of pension

One of the most common appeals that I have walked clients through is in the retirement year. Since Medicare premiums are based on your income from two years ago, it is not uncommon for high earners who retire after 63 to have one year of increased premiums. You can appeal this premium by stating that you retired and estimating your projected post-retirement income.

While these surcharges can come unexpectedly and be a painful “tax” to pay, understanding them and planning in advance can help avoid surprises. In many cases, it may make sense to accept the surcharge for a few years in order to accelerate income and enjoy many other years without it.

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.