Calculating Your Minimum Lifestyle Floor

I was recently listening to a financial advisor describe the “minimum lifestyle floor” (MLF) that they have their clients calculate. The idea is that your expenses can be divided into two categories, necessities, and fun money. The necessities include food, housing, basic transportation, utilities, and health care. I also would add another “other” category for things like basic charitable giving, small gifts, personal care, and pets since you’re probably not going to pass on Christmas gifts or give away Buddy the dog because your finances are tight.

It’s important to keep in mind that for necessities, you likely want more than just a basic level, which is where the “minimum lifestyle” works itself into the equation. You need to answer, “How much would I need to spend in these areas in order to maintain a lifestyle I would be proud of throughout retirement?” The answer is probably close to what you spend now with some inflation increases along the way.

These expenses should ideally never be sacrificed throughout retirement, and you should design an investment portfolio around that. To do that, those expenses should be covered by guaranteed or predictable income streams – such as Social Security, pensions, annuities, or conservative income streams. Only then do you take risks to fund fun expenses above and beyond your MLF. Having a comfortable lifestyle funded by a predictable income stream is also likely to aid in good investment behavior during bear markets because you can sleep well at night knowing your retirement income needs are not in jeopardy. Maybe you miss a vacation for a year or donate a little less to your alma mater, but most of us can get on just fine with these small sacrifices.

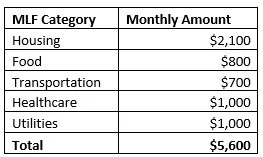

Here’s an example of how this might work. Jim and Jane retire and calculate their MLF to be $5,600/month with $4,000/month for flexible fun money for total spending of $9,600/month.

After calculating their minimum lifestyle floor and guaranteed income sources, they need to fund another $700/month from either an annuity or by using conservative estimates for bond or stock dividend income streams.

One step beyond this is to run forecasts into the future for how this MLF will increase over time and how much will be needed to fund it at that time using inflation estimates for each MLF category and income source. With a certain bias, this is where the assistance of a financial planner can be helpful!

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.